While financial institutions are spending time and resources to find out how much business they can gain by adopting blockchain technology, corporations are taking a more cautious approach.

While financial institutions are spending time and resources to find out how much business they can gain by adopting blockchain technology, corporations are taking a more cautious approach.

If corporations start working on blockchain projects, it will be for mission-critical (i.e., niche) applications, while waiting for the “big thing” to occur. Banks, in fact, may not have any role to play in their future plans for the technology.

Why are corporations showing little interest in blockchain?

Corporations are late to take on the blockchain debate, and their lack of awareness may be the symptom of a simple lack of interest. After all, banks are all over blockchain because bitcoin shook them up and made them keep their eyes wide open.

Another possible explanation for such slow corporate uptake is that one of blockchain technology’s value propositions, if not the main one, is that buyers and suppliers can connect directly and form online networks, removing the need for middlemen.

Smart contracts running on the blockchain should automatically detect trigger events along the trade value chain and instruct parties on actions to take to comply with contractual obligations. This sets the blockchain as the enemy of all intermediary operators in a business-to-business (B2B) environment.

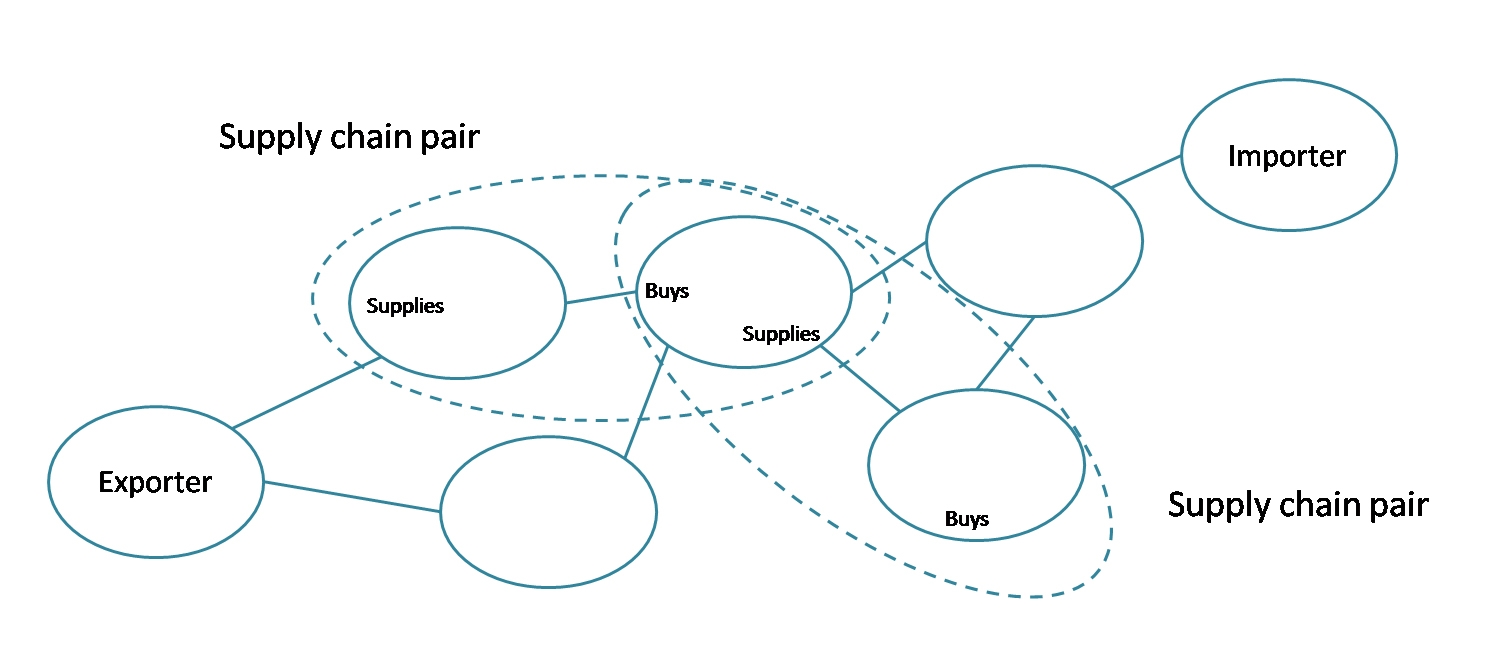

A B2B relationship is made of a sequence of buyer and supplier pairs (Figure 1), with a relatively high level of trust between the two.

Figure 1: B2B Supply Chain Pairs

Source: Aite Group

While there can be very little trust between an exporter and an importer at the edges of the B2B value chain, this is certainly not the case between the paired parties. So if each pair on the B2B value chain intrinsically trusts each other, what additional contribution could a blockchain bring?

Furthermore, there is a clear shift to trade on open account terms, and open account business is increasing in market share. Open account occurs when a seller ships the goods and all the necessary shipping and commercial documents directly to a buyer, who agrees to pay the seller’s invoice at a future date.

Open account is typically used between established and trusted traders. That has compelled the banking industry to seek to re-engage with buyers and suppliers. They are doing this by developing a blockchain-based value proposition aimed at meeting the needs of traders operating on these open account terms.

But, if open account transactions are founded on trust and keep banks out of the picture, why should corporate trade partners want to get them back with a blockchain? Since open account transactions are based on the principle of trust between parties, why the need for a trust-free distributed ledger technology?

Challenges ahead of full blockchain implementation

Additional challenges present the need to examine prior use evidence before B2B partners can fully adopt blockchain applications:

- Nobody runs totally digital flows end to end. How does one manage the transition of ownership between data encrypted in a block in the chain and paper-based documents?

- Companies (e.g., logistics service providers) are making money on paper-based trade, so why should they change to digital?

- Trade finance is frequently referred to as the domain that would most benefit from blockchain applications. But trade finance partnerships are already established on trust, so why the need to change?

- Freight forwarders are taking care of paper-intensive customs business on behalf of their clients. The service allows the client to outsource a significant portion of logistics clearance and controls activities, making it a highly profitable business to the service provider. Since all parties are enjoying the benefits of a de facto situation, why should they replace that service with paperless blockchain applications?

Is secrecy the enemy of blockchain?

To summarize, the blockchain is presented today as the enemy of all intermediary business, as it eliminates the need to have a central controlling entity responsible for safekeeping trading records.

If there was to be industry-wide adoption of blockchain, the role of this controlling entity would be replaced by a decentralized ledger that no one single party owns or controls. This apparent advantage may backfire and be counterproductive to corporations.

The untold truth is that the last thing corporations may want is to give total visibility of their trade transactions. The existence of a publicly distributed ledger may not represent the best commercial interest for B2B partners.

There is the problem of revealing too much information: A company does not want its competitors to know where it’s getting goods. Commercial confidentiality is the most important element to preserve.

Blockchain adoption dependent on a wait and see approach

Innovation happens in bursts. When the Internet became popular, two “asteroids” hit the consumer world: email and the Web browser. Such a disruptive effect from blockchains has not yet occurred in the corporate world.

While the bitcoin has been the killer app (i.e., the asteroid) for banks, there is nothing for corporations with the same mass adoption scale as bitcoins – yet. If this is the case, then little or no demand for blockchain-based applications can be expected by corporate users.

Maybe those most aware of the technology within corporations are financial directors and corporate treasurers, for the simple reason that they are frequently exposed to banks and therefore absorb the inherent dynamics. These corporate representatives expect changes in payments, securities trade, and bank clearing.

All have concerns that the blockchain discussion is moving too fast, however. The corporate side of the equation needs to first see a consolidation of the different players that populate the crowded space of blockchain applications. The need for standards and regulation is the next call.

disqus comments